National Financial Accounts Bulletin by Institutional Sector – Fourth Quarter 2025

Below is a summary of the financial accounts by institutional sector and financial instrument. For further details, please refer to the Technical Bulletin (only in Spanish).

Note: Starting with this bulletin, the series of consolidated balances with counterpart sectors is published for the first time for the period Q1 2022 to Q4 2024. As a result of this new counterparty estimation, the non-consolidated balances for Q1 2022 to Q4 2024 were revised, and the non-consolidated balances for Q1 2025 to Q3 2025 were re-estimated based on the new non-consolidated balance for Q4 2024.

Financial Flows for the fourth quarter of 2025

1. By institutional sector

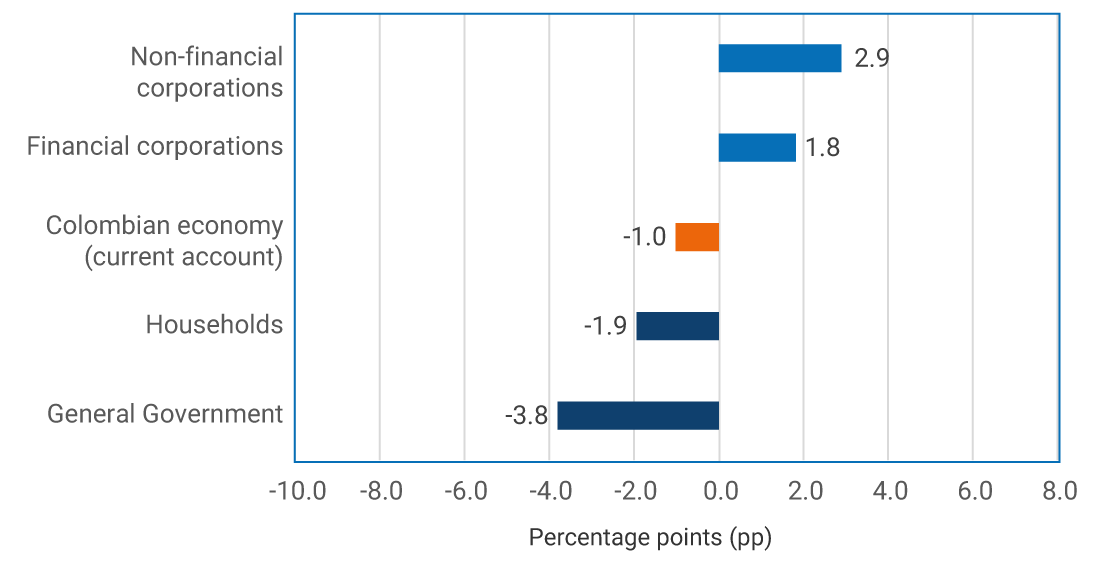

According to the financial accounts calculated by Banco de la República (the Central Bank of Colombia), in the fourth quarter of 2025, the current account deficit of the Colombian economy reached 2.7% of quarterly Gross Domestic Product (GDP), compared to 1.7% in the same period in 2024. This is primarily explained by the deficits of the General National Government (-20%). The institutional sectors that partially offset the deficit were non-financial corporations (12.7%), households (3.8%), and financial corporations (0.7%).

Compared to the fourth quarter of 2024, the economy’s consolidated external financing needs increased by 1.0 percentage points (pp), as reflected in the internal and external financing flows of institutional sectors. Therefore, the increase in the economy’s financing was explained by the greater financing needs of the General National Government (3.8 pp) and by changes in the financing capacity of households (-1.9 pp), as well as non-financial corporations (2.9 pp) and financial corporations (1.8 pp).

2. By financial instrument / net external financing

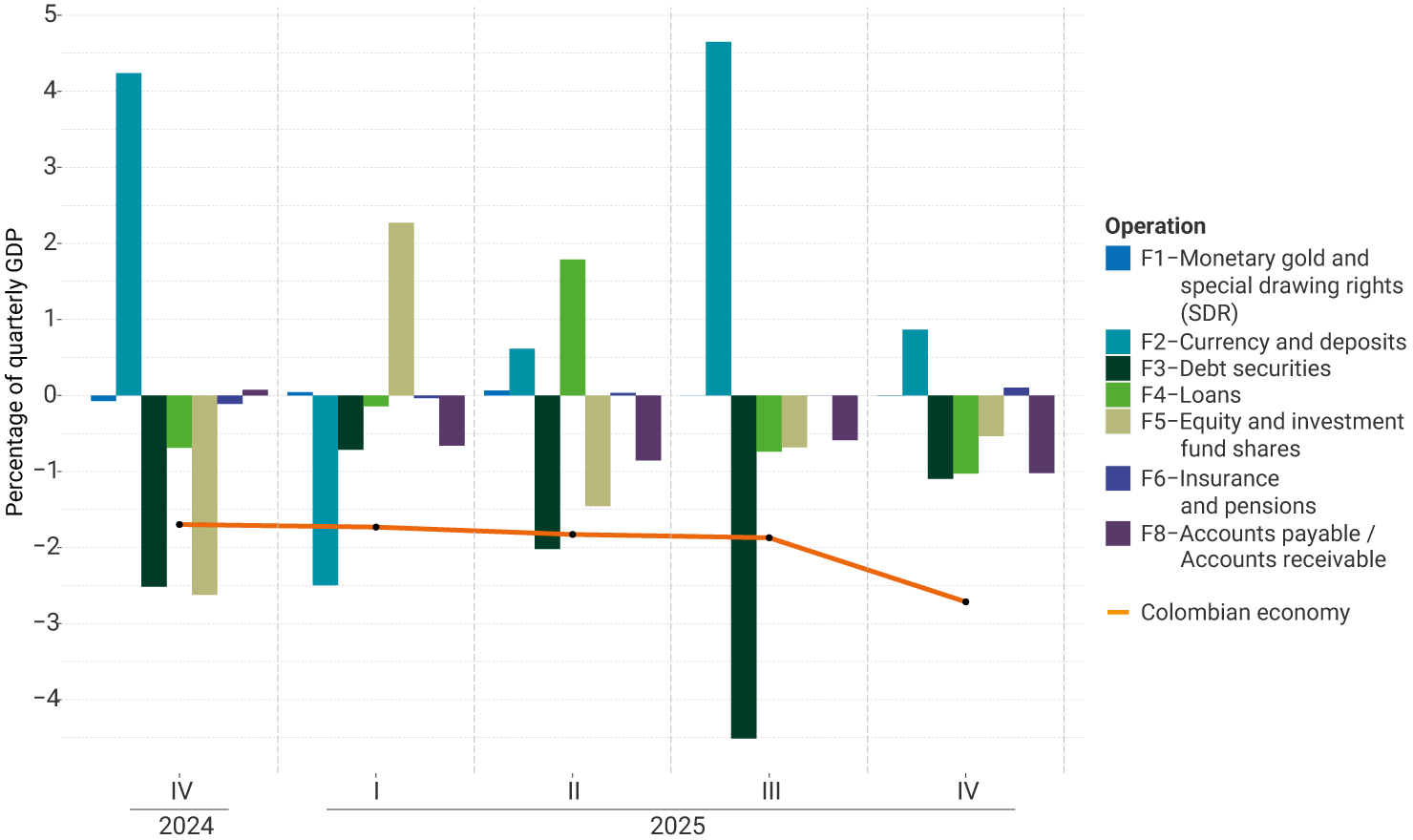

The negative quarterly saving-investment balance of the Colombian economy was covered by net external financing flows equivalent to 2.7% of quarterly GDP. Net inflows of financial resources from the rest of the world were primarily channeled through the issuance of debt securities to the rest of the world (1.1%), the incurrence of loans (1.0%), and accounts payable (1.0%). This was partially offset by deposit outflows to the rest of the world, totaling 0.9% of quarterly GDP.

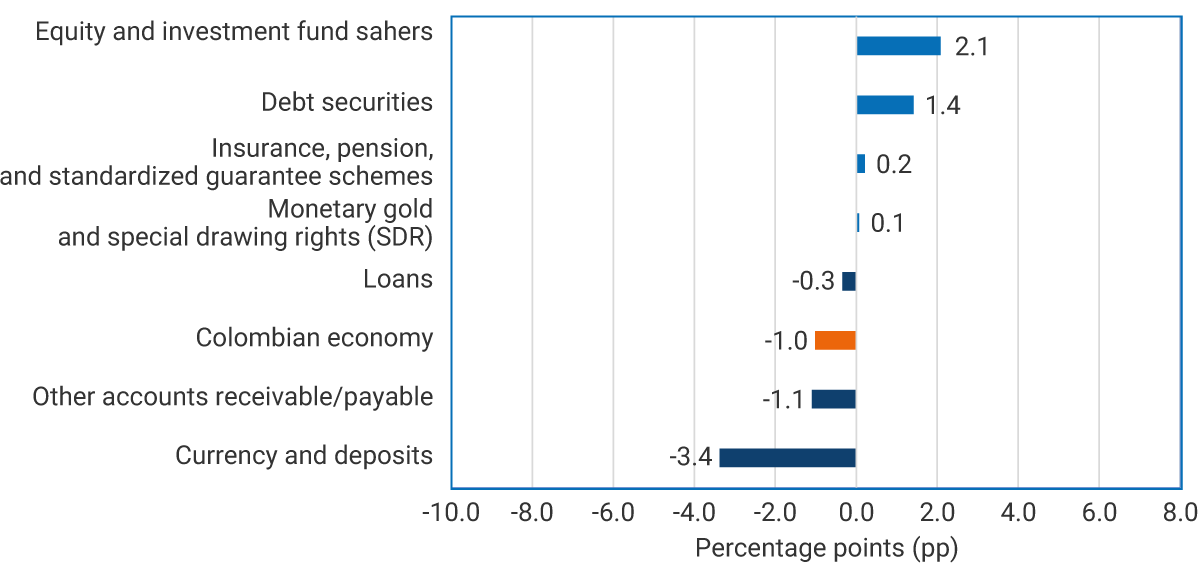

Compared to the fourth quarter of 2024, the 1.0 pp increase in external financing inflows was primarily driven by a lower accumulation of deposits abroad (3.4 pp) and a higher incidence of accounts payable (1.1 pp). This was partially offset by a decline in equity investments (2.1 pp) and a lower issuance of debt securities abroad (1.4 pp).

Financial Account Balances for the fourth quarter of 2025

1. Net financial position by institutional sector

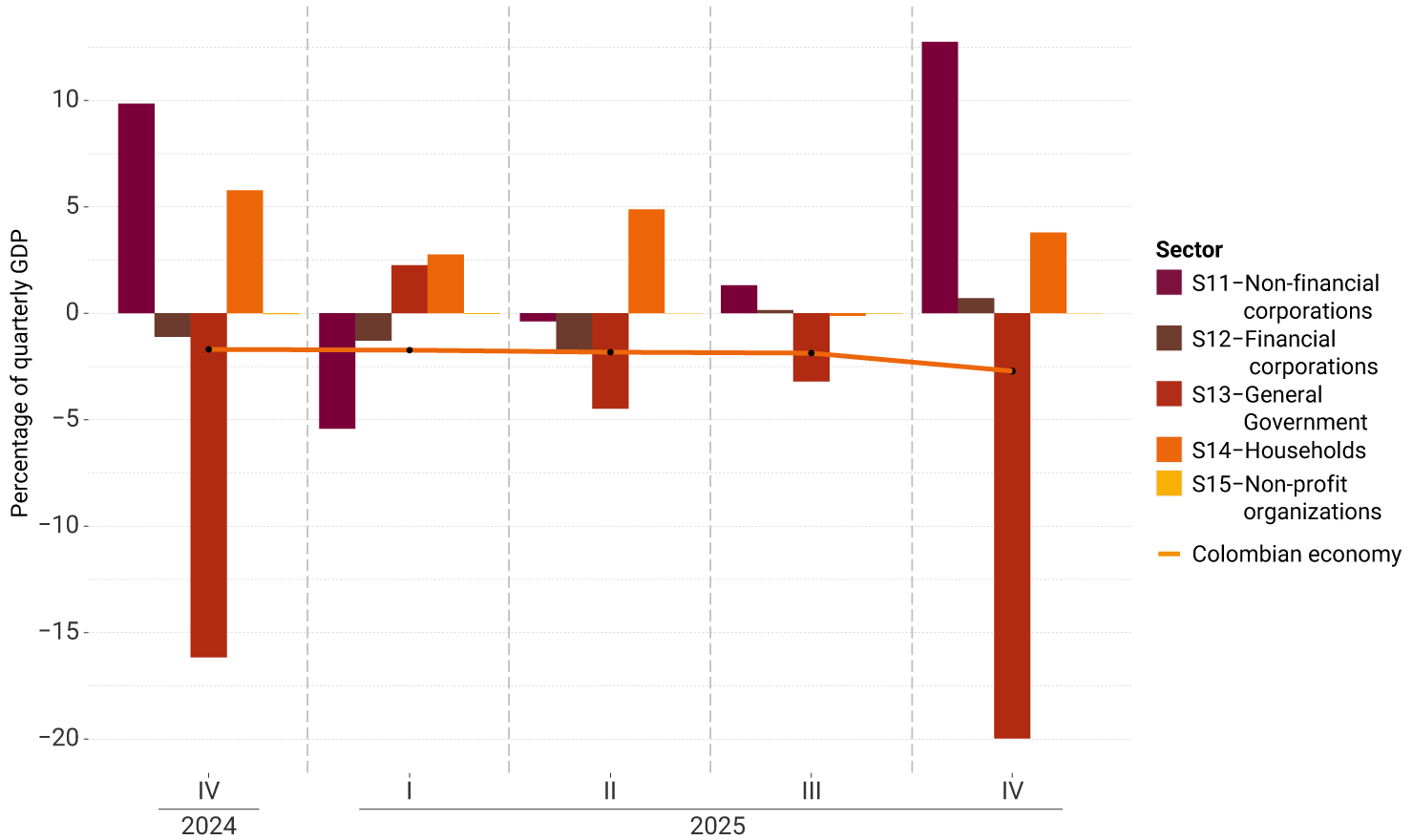

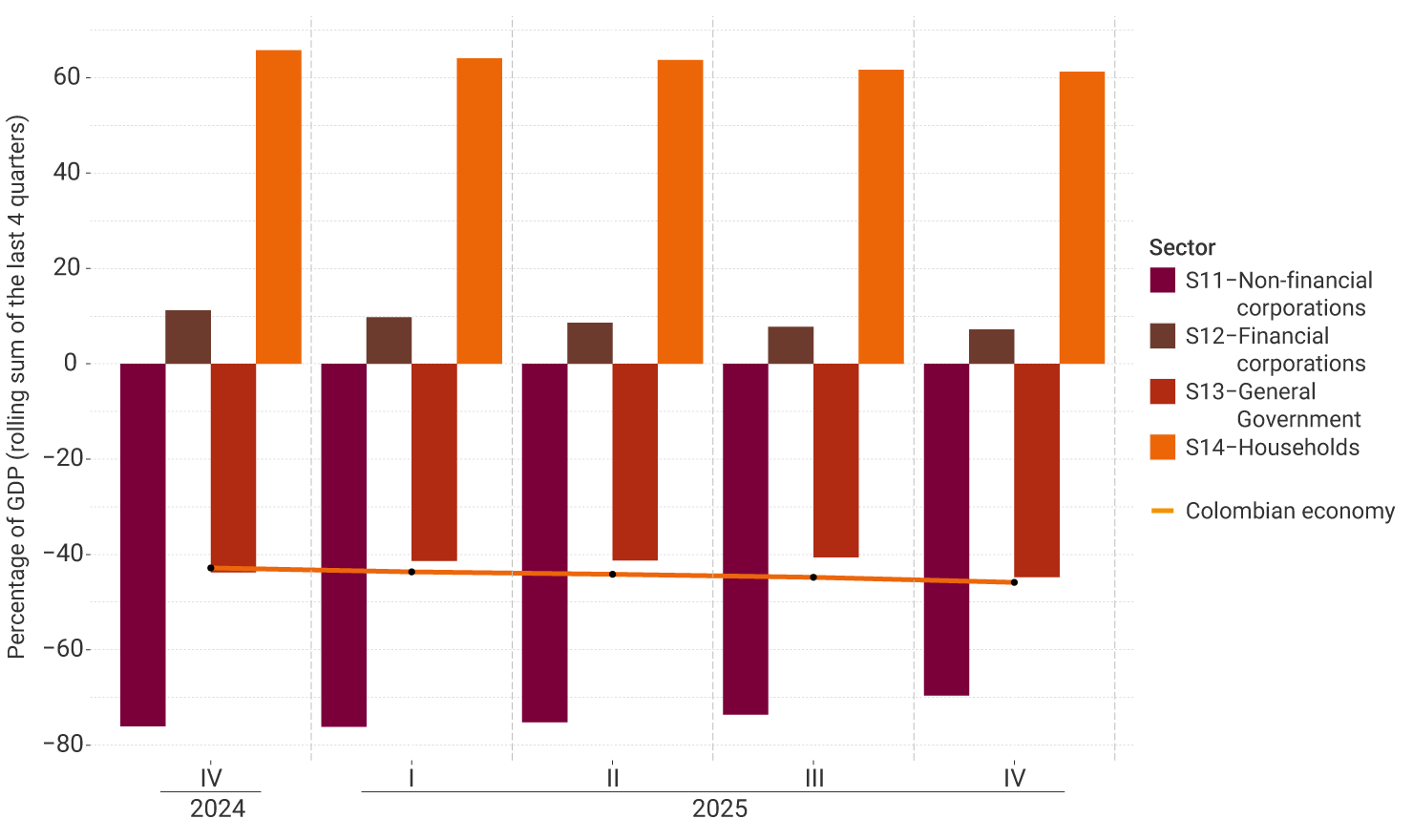

At the end of 2025, the Colombian economy recorded a net debtor position with the rest of the world equivalent to -45.9% of annual GDP. The sectors with net debtor positions were non-financial corporations (-69.6%) and the General National Government (-44.8%). In contrast, households (61.1%) and financial corporations (7.2%) showed net creditor positions.

Between 2024 and 2025, there was an increase of 3.0 pp in the economy’s external debtor position, explained by lower net creditor positions of households (4.5 pp) and financial corporations (4.0 pp), together with a larger debtor position of the General National Government (1.0 pp). These changes were partially offset by a reduction in the net debtor position of non-financial corporations (6.5 pp).

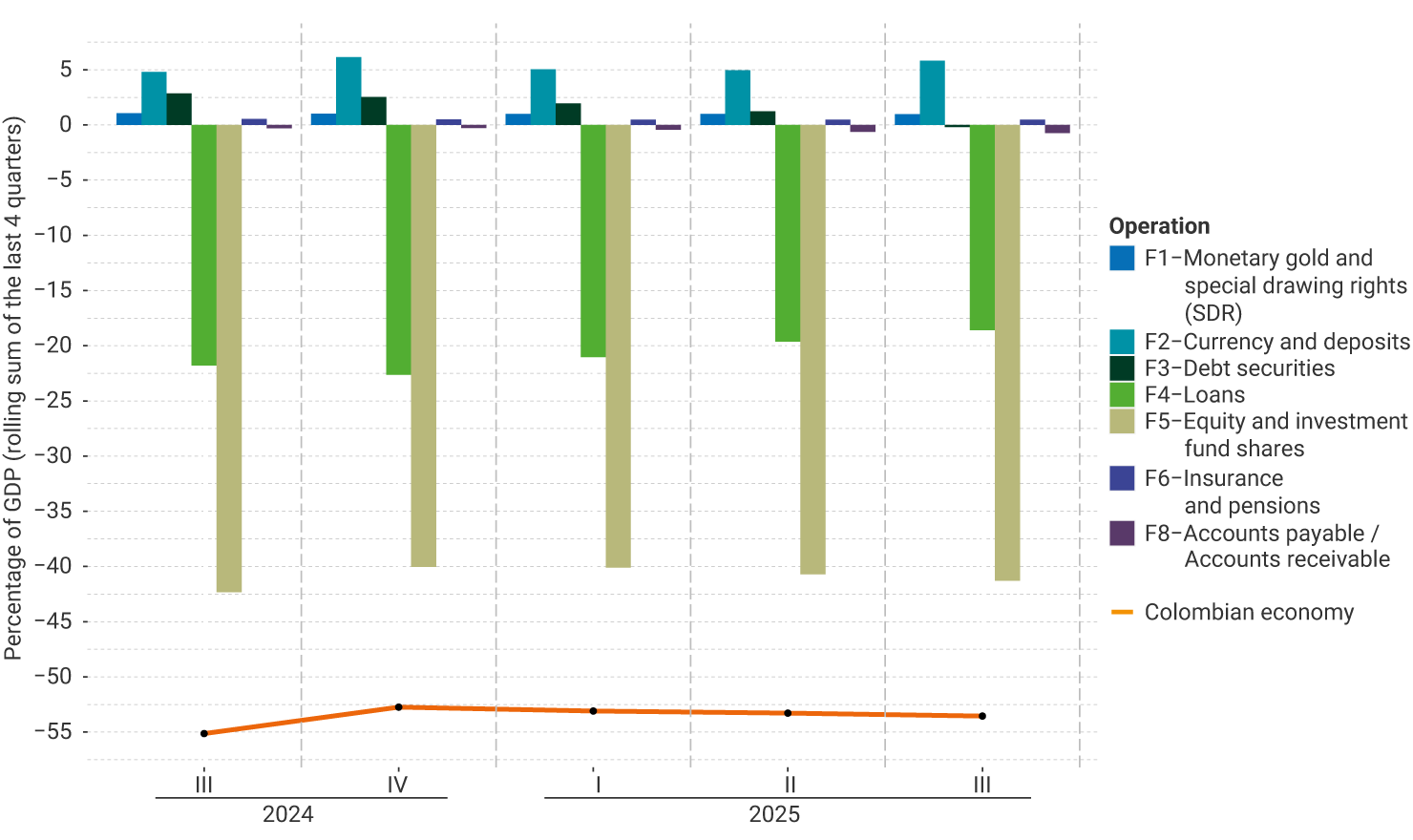

2. Net external position by financial instrument

At the end of 2025, the net debtor position of the Colombian economy with the rest of the world, equivalent to -45.9% of annual GDP, was primarily represented by equity investments (-31.6%), loans (-17.1%), and debt securities (4.2%). This was partially offset by Colombians’ foreign holdings of deposits (5.9%).

Between 2024 and 2025, the 3.0 pp increase in the economy’s net debtor position was mainly driven by the growth of debtor positions in equity investments (3.8 pp) and debt securities (2.4 pp). This change was partially offset by a lower debtor position in loans (4.5 pp).