Report of the Board of Directors to the Congress of Colombia – March 2026

Pursuant to Article 5 of Law 31 of 1992, the Board of Directors of Banco de la República (the Central Bank of Colombia) submits a report to the Honorable Congress of Colombia, informing about the performance of the economy and its outlook. This report is submitted twice a year, in March and July, within ten business days following the start date of the sessions of the Congress.

Gross domestic product (GDP) growth in Colombia reached 2.6% in 2025, exceeding the figures recorded in 2023 (0.8%) and 2024 (1.5%). However, this outcome fell below projections from both market analysts (2.8%) and the technical staff of Banco de la República (the Central Bank of Colombia) (2.9%). Regarding inflation performance in 2025, the Bank’s technical staff, the members of the Board of Directors (BDBR), and analysts had expected inflation to continue its downward trend observed in 2024, moving closer to the 3.0% target. However, this did not materialize. By the end of 2025, headline inflation stood at 5.1%, only slightly below that recorded at the end of 2024 (5.2%). On the other hand, Colombia’s unemployment rate continued to decline in 2025, reaching 8.5% in the fourth quarter. Meanwhile, net foreign reserves totaled USD 66,352 million (m) at the end of 2025, representing an increase of USD 3,871 m compared to their level observed at the end of 2024. In addition, Banco de la República reached a new historic profit of COP 13.9 trillion.

Macroeconomic Environment

- Global economy in 2025 was marked by an environment of high political and trade uncertainty, driven by the imposition of new tariffs by the United States.

- However, partial trade agreements between the US and other major economies were reached over the course of the year, helping to ease tariff-related uncertainty and mitigate some of these effects.

- Across Latin America, growth was heterogeneous and generally moderate, in contrast to the stronger dynamism of several emerging Asian economies, which exceeded the global average.

- In both advanced and emerging economies, inflation continued to ease throughout 2025. Lower cost pressures compared to previous years, together with still-restrictive monetary policies and a gradual normalization of labor markets, contributed to this price adjustment trend.

- The recently initiated war in Iran, which has rapidly spread to other countries in the Middle East, cast a new layer of uncertainty over the outlook for global growth, inflation, oil prices, international trade, and many other macroeconomic and financial variables. As a result, oil prices have exhibited significant volatility.

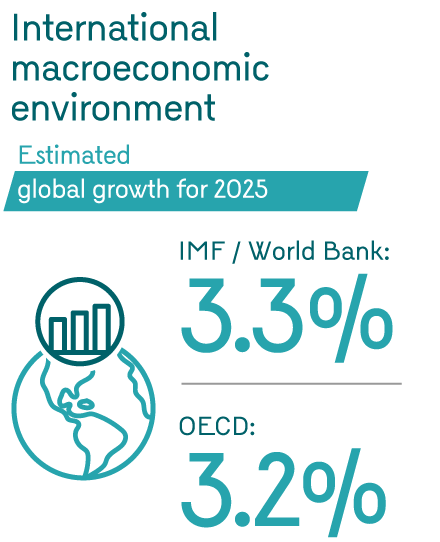

- In their most recent report, the International Monetary Fund (IMF) and the World Bank estimate global growth at 3.3% for 2025, while the Organization for Economic Cooperation and Development (OECD) estimates growth of around 3.2%, which does not incorporate recent geopolitical developments.

Economic Activity in Colombia

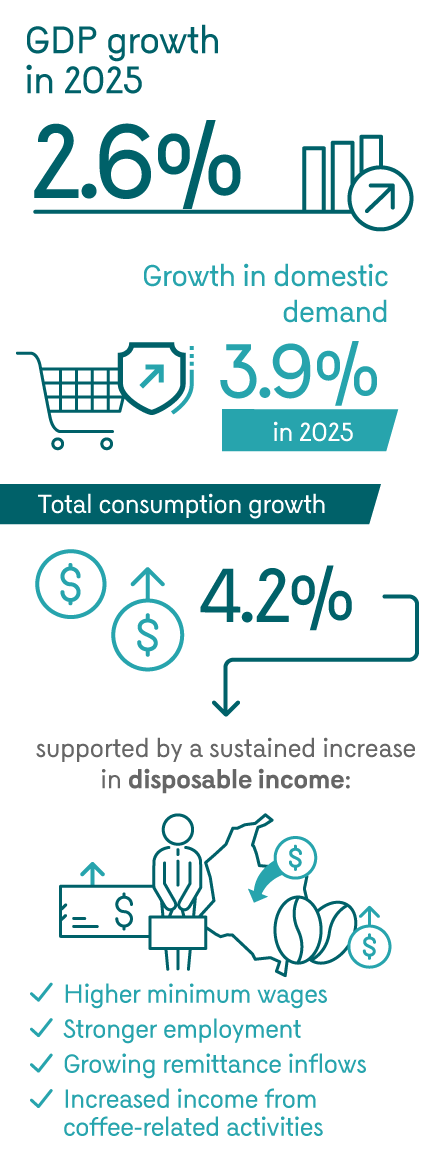

- In 2025, Colombia’s GDP grew by 2.6%, surpassing the figures recorded in 2023 (0.8%) and 2024 (1.5%). This outcome occurred within the context of an expansionary fiscal policy.

- Domestic demand remained strong, growing at an average rate of 4.4% annually during the first three quarters of the year and 3.9% for the year as a whole.

- Regarding the composition of demand, a bias toward overall consumption was observed, which increased by 4.2%. Household consumption expanded by 3.6%, driven primarily by durable goods, which typically have a high imported component. This is supported by a sustained increase in disposable income, resulting from higher minimum wages, stronger employment levels, a growing inflow of workers’ remittances, and increased income from coffee-related activities.

- Fixed investment grew by 1.3% in 2025. The main driver was investment in machinery and equipment, which boosted imports of capital goods throughout the year. In contrast, housing investment contracted by 6.5% from the already low levels observed in the previous year due to lower completion of construction projects in both the Low-Income Housing (LIH) and non-LIH segments.

- On the productive sector side, artistic, entertainment, and recreational activities were the most dynamic, expanding by 9.9% over the year, followed by trade and public administration and defense. In contrast, mining and quarrying was the sector with the sharpest decline, contracting by 6.2% year-on-year, followed by a 2.8% contraction in the construction sector, driven mainly by building activities.

- For 2026, Banco de la República’s technical staff expects GDP growth to be somewhat lower than in 2025. This outcome is likely to be partly driven by less favorable external conditions, given slower growth in remittances and in earnings from coffee exports, as well as the uncertain effects of the recent armed conflict in the Middle East.

- The cumulative effects of a restrictive monetary policy, aimed at moderating the pace of domestic demand growth to levels consistent with inflation converging toward its target, are also expected to constrain the rate of economic activity.

Employment

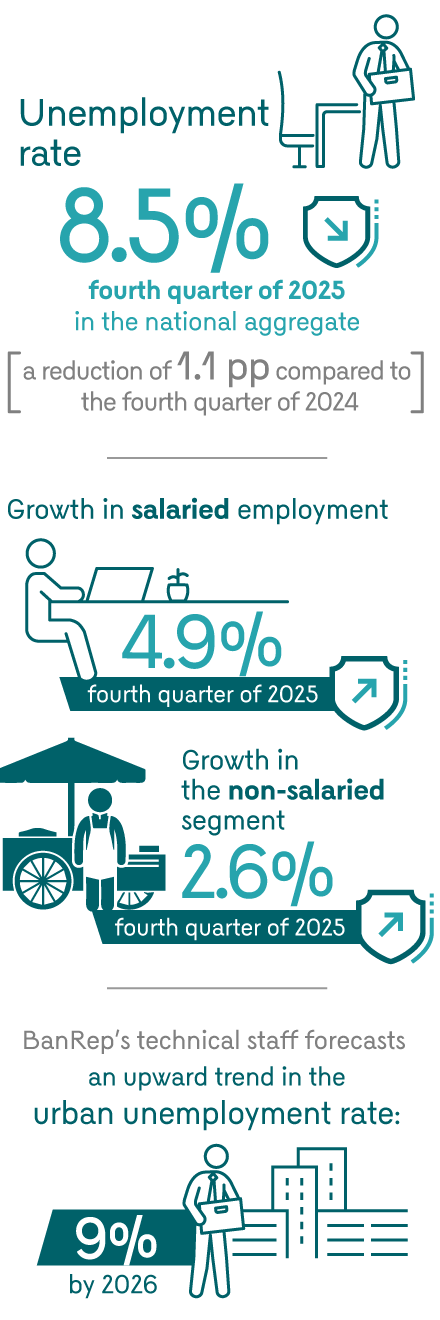

- In 2025, Colombia’s unemployment rate continued to decline. Between the last quarter of 2024 and the same period of 2025, this rate fell by 1.1 percentage points (pp) in the national aggregate, bringing unemployment nationwide to 8.5% in the fourth quarter of the year.

- By geographical areas, the reduction in the unemployment rate was similar across urban areas, other municipalities, and rural areas, standing at 8.7% and 8.2%, respectively.

- By gender, unemployment rates stood at 6.6% and 11.1% respectively, for men and women in the fourth quarter of 2025, leaving the gender gap relatively stable at around 4.5 pp, a level below that observed before the pandemic.

- Salaried employment grew by 4.9% in the fourth quarter of 2025, while the non-salaried segment increased by 2.6%.

- For most of 2025, the informality rate declined to a historically low level; however, starting in the fourth quarter, it rebounded, standing at 55.8% during that period. This late-year growth in informality is consistent with the increase in non-salaried employment, a segment that is predominantly informal.

- By economic sector, the largest annual increases in informality as of the fourth quarter were recorded in industries such as mining, electricity, gas and water, and finance. On the other hand, the most significant reductions in the informality rate were observed in professional activities and in the agricultural sector.

- The hiring expectations balance reported in Banco de la República’s Quarterly Survey of Economic Expectations turned negative in January 2026, after posting positive results during 2025.

- Forecasts from the Bank’s technical staff are consistent with this signal, suggesting an upward trend in the urban unemployment rate, which is expected to average 9.0% in 2026.

Inflation

- Inflation in 2025 performed very differently from that observed a year earlier. In the first half of the year, it stopped declining, and at the beginning of the second half, it began to trend upward, rising from 4.8% in June to 5.5% in October, before easing slightly and reaching 5.1% by the end of 2025, very close to the level observed at the end of 2024.

- Similarly, core inflation (excluding food and regulated items) showed downward rigidity, standing at 5.0% in December 2025, only slightly below that figure recorded in December 2024 (5.2%).

- This performance was mainly driven by the strengthening of domestic demand, which grew at an average rate of 4.4% in the first three quarters of the year and 3.9% for the year as a whole, in response to growth generated by increased private and public spending.

- In addition, a growing process of price indexation contributed to this trend, stimulated by rising inflation expectations and increases in the minimum wage, which rose by 11% in 2025, including transport allowance, a figure that doubled the inflation observed in 2024.

- Inflation in regulated items declined from 7.3% to 5.4% between 2024 and the end of 2025, although it remained above the inflation target due to significant adjustments in transportation, education, and gas tariffs, among other factors.

- In January 2025, headline inflation and core inflation expectations by December 2026 were 3.6% and 3.3%, respectively, reflecting their confidence that inflation would continue a downward path, gradually converging toward its target over a two-year horizon.

- These expectations gradually increased as analysts noted the persistent downward rigidity of inflation over the course of 2025. Thus, by December 2025, analysts had revised their expectations for headline and core inflation for the end of 2026 to 4.6% in both measures.

- However, the strongest shock came with an increase in the minimum wage for 2026, set at just over 23%, which led analysts in January 2026 to further raise their year-end 2026 expectations to 6.4% for headline inflation and 6.7% for core inflation.

- When comparing these latest expectations with those held by analysts in December 2025, this shows that the upward revision for year-end 2026 amounted to 180 basis points (bps) for headline inflation and 210 bps for core inflation.

Monetary Policy

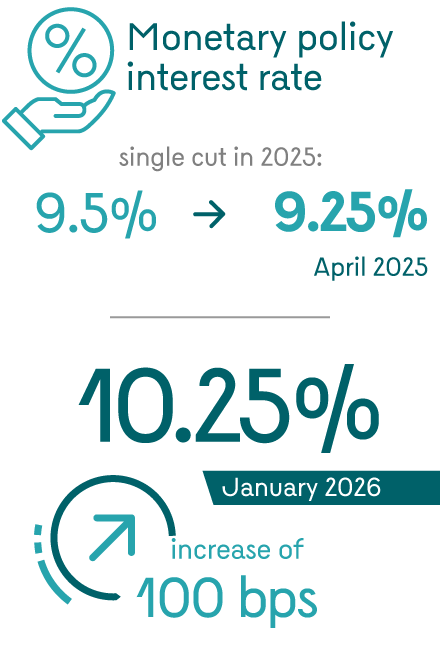

- The evolution of inflation and inflation expectations in 2025 did not provide appropriate conditions to continue reducing the monetary policy interest rate that had been undertaken in 2024. The only cut in the monetary policy interest rate in 2025 was implemented at the late-April meeting of the BDBR, when it was reduced from 9.5% to 9.25%.

- When comparing the increase in analysts’ expectations in January 2026 with those in December 2025, the BDBR, at its January meeting, decided by majority vote to raise the monetary policy interest rate by 100 basis points, to 10.25%. This increase, although significant, was insufficient to offset the reduction in the real ex-ante interest rate resulting from the upward revision of inflation expectations.

- In the minutes of the January meeting of the BDBR, the members of the majority group stated that this was an essential decision to prevent a persistent de-anchoring of inflation from the target and to address the serious risk of eroding the monetary authority’s credibility regarding its commitment to the inflation target and its ability to fulfill its constitutional mandate.

Balance of Payments

- The country’s current account of the balance of payments recorded a deficit of USD 10,883 m in 2025, which was USD 3,871 m higher than that recorded a year earlier. This imbalance was equivalent to 2.4% of GDP, a figure 0.7 pp higher than in 2024.

- By components of the balance of payments, this current account deficit was driven by negative balances in trade in goods and services (USD 14,871 m) and in net primary income outflows (USD 12,446 m), which were partially offset by a positive balance in current transfers (USD 16,435 m).

- The goods trade balance deficit in 2025 increased by USD 5,677 m compared to the previous year, as the 0.8% rise in exports (USD 406 m) was more than offset by a 10.1% increase in the value of imports (USD 6,082 m).

- The increase in goods exports was driven primarily by coffee, industrial products (particularly chemicals and food products), and gold exports, whose growth was offset by lower sales of crude oil and its derivatives, as well as coal.

- Regarding imports, their increase was mainly driven by higher external purchases of consumer goods and by inputs and capital goods for industry, partially offset by lower imports of fuels and lubricants.

- Colombia’s terms of trade improved by 5.9% in 2025 compared to the previous year. This performance was mainly driven by increases in international prices of coffee and gold, as well as a decline in the US dollar price of imports. These factors more than offset the decline observed in oil prices.

- During 2025, the country’s financial account recorded net capital inflows of USD 9,047 m (2.0% of GDP), a figure USD 3,470 m higher than the one observed in 2024.

- Among these inflows, resources from foreign direct investment (FDI) stood out, amounting to USD 11,469 million (2.5% of GDP), USD 2,215 million lower than the previous year. These resources were channeled primarily into the financial and business services sectors, mining and oil, manufacturing industry, trade and hotels, and electricity.

- For 2026, the technical staff projects a moderate widening of the current account deficit relative to the previous year, amid high uncertainty due to ongoing international geopolitical conflicts.

Public Finance

- According to the update of the 2026 Financial Plan (FP-26) published by the Ministry of Finance and Public Credit (MHCP in Spanish), the total deficit of the Central National Government (CNG) decreased from 6.7% to 6.4% of GDP between 2024 and 2025, reaching an amount of COP 117.8 trillion (t). This reduction was achieved solely due to a lower interest burden, which was partially offset by an increase in primary expenditure.

- Compared to the projection set out in the 2025 Medium Term Fiscal Framework (MTFF 25), the total deficit of the CNG was 0.8 pp of GDP lower.

- The CNG's primary deficit increased from 2.4% to 3.5% of GDP between 2024 and 2025, reaching COP 65.7 t.

- In line with the higher primary deficit, the CNG's gross debt increased from 61.3% of GDP in 2024 to 64.4% in 2025. This performance was explained by a higher stock of gross domestic debt as a share of GDP, which increased by 5.0 pp, in contrast to foreign debt, which declined by 1.9 pp of GDP, partly due to the peso's appreciation.

- Despite the increase in gross debt, the CNG's net debt declined from 59.0% to 58.5% of GDP between 2024 and 2025, largely due to treasury operations, through which the Government accumulated both domestic and foreign assets.

- The MHCP projects a total CNG deficit of 5.1% of GDP and a primary deficit of 2.1% of GDP in 2026, both lower than the deficits observed in 2025.

Foreign Reserves

- Net foreign reserves totaled USD 66,352 m at the end of 2025, up USD 3,871 m from the end of 2024. This increase was explained by the positive returns earned during the year.

- The return on foreign reserves in 2025, excluding the exchange-rate component, stood at 4.76% (USD 3,067 m), mainly driven by higher interest rate levels, which boosted foreign reserve profitability through increased interest income from investments.

- The return was also supported by the appreciation of investments amid a decline in short-term interest rates in the main markets where the reserves are invested, and by the appreciation of other reserve currencies against the U.S. dollar, which generated a positive exchange-rate effect on their valuation.

- According to the IMF methodology for evaluating the level of reserves to cover balance of payments risks, Colombia maintains an adequate level, with a ratio of 1.24 in January 2026, indicating that reserves are sufficient to face extreme external scenarios.

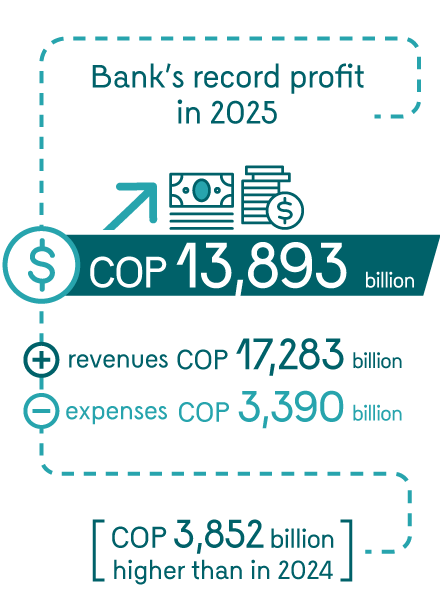

Profits of Banco de la República

- Banco de la República's profit in 2025 reached a new historical record of COP 13,893 billion (b), as a result of revenues of COP 17,283 b and expenses of COP 3,390 b.

- This profit was COP 3,852 b higher than the one observed in 2024, driven by higher revenues and lower expenses.

- Revenues were mainly from the return on foreign reserves, which amounted to COP 11,894 b, an increase of COP 2,555 b compared to 2024.

- For 2026, a profit of COP 11,271 b is projected, which is COP 759 b higher than that assumed in the approved 2025 budget, in an economic environment that would support the profitability of foreign reserves.

Boxes

Box 1. Potential effects of the increase in the minimum wage on inflation (only in Spanish)

Box 2. Inflation expectations and their recent evolution (only in Spanish)

Box 4. Colombia’s foreign trade basket of goods and services: recent trends (only in Spanish)