Monetary Policy Report - April 2026

The Monetary Policy Report presents the Bank's technical staff's analysis of the economy and the inflationary situation and its medium and long-term outlook. Based on it, it makes a recommendation to the Board of Directors on the monetary policy stance. This report is published on the second business day following the Board of Directors' meetings in January, April, July, and October.

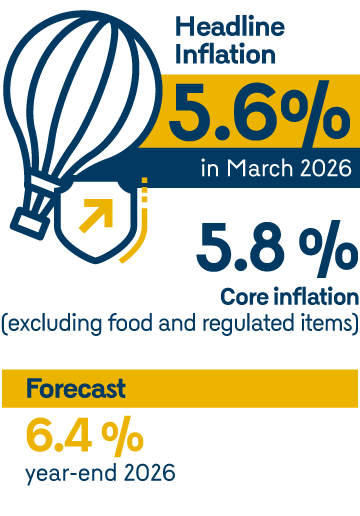

During the first quarter, annual headline inflation (5.6%) increased and moved further away from the 3% target. Different economic agents expect inflation to continue increasing over the remainder of the year. Economic growth has moderated, but the level of country spending remains high and exceeds the long run sustainable level. The domestic demand continues to be driven by strong household consumption and fiscal stimulus of the government, among other factors. In this context of excess demand and inflation expected to continue increasing in 2026, the Board of Directors of Banco de la República raised the policy interest rate to support the convergence of inflation toward the 3% target in 2027. This decision reaffirms the commitment of Banco de la República to its constitutional mandate to maintain the purchasing power of the currency and achieve the highest possible sustainable level of output and employment.

Inflation continued to rise in the first months of the year and moved further away from its target, driven by higher labor costs, strong domestic demand, and disruptions in the production of some goods. Additional increases in inflation are expected throughout the year; however, monetary policy actions would allow inflation to decline again and approach the 3% target in 2027, amid high global and domestic uncertainty.

- In March, headline inflation stood at 5.6% and core inflation, which excludes volatile components such as food and regulated items, at 5.8%. In both cases, inflation was above its December level and continued to move further away from the 3% target.

- The acceleration of prices in the first quarter of the year is explained by increases in labor costs following reflected in significant wage hikes; economic activity that remains strong and continues to show signs of excess spending; disruptions in food production related to adverse weather conditions and road blockages; and higher costs of international goods and inputs as a result of the conflict in the Middle East.

- Inflation did not increase further due to downside surprises observed in the first months of the year in some regulated prices, such as gas, electricity, and fuels, as well as a lower exchange rate.

- Inflation expectations of different economic agents (analysts, business, trade unions, academics, and investors in the government debt market) have increased since late 2025 and remain above the 3% target.

- Inflation is expected to continue increasing throughout 2026 and reach 6.4% in December 2026. In 2027, inflation is expected to decline and gradually move closer to the 3% target, supported by the monetary policy decisions taken by Banco de la República.

- The prolongation of the conflict in the Middle East could result in further upward pressures on international energy prices, fertilizer prices, and the international prices of some goods, as well as in less favorable financing conditions for the country.

- The expected inflation remains surrounded by high uncertainty due to developments in the conflict in the Middle East, exchange rate behavior, the magnitude of the impact of the minimum wage increase, possible adverse weather conditions, and adjustments in the prices of certain regulated goods and services, among others.

The Colombian economy grew by 2.6% in 2025, mainly driven by strong household consumption, the government fiscal deficit, and a robust labor market, while investment remained behind. For 2026, more moderate economic growth is expected in a highly uncertain global environment.

- In 2025, the economy grew 2.6%, mainly driven by household consumption and the stimulus represented by the high fiscal deficit.

- Household consumption remained high, supported by growth in inflows of remittances, strong performance of income from coffee sector, recovery in credit, low unemployment, and, in the short term, higher wages.

- Investment showed weak performance due to lower dynamism across all its components (machinery and equipment, and housing and infrastructure construction).

- Employment continued to expand, and the unemployment rate remained at historically low levels. However, employment growth in urban areas has been moderating.

- Towards the end of 2025 and in the first months of the year, economic activity slowed, partly due to transitory disruptions in the production of some sectors.

- In 2026, the economy is expected to continue growing (2.4%), with consumption remaining dynamic supported by a persistent fiscal deficit, strong foreign tourism, favorable labor market conditions, and expectations of high oil and coal prices. In contrast, remittances and income from the coffee sector would contribute less to economic growth. These factors, along with the effects of transitory production disruptions, would result in a more moderate pace of growth.

- In 2027, economic growth would be somewhat lower than in 2026, in the context of a less dynamic external income and the accumulated effects of monetary policy, consistent with inflation returning to its target.

- These projections remain highly uncertain, associated with the conflict in the Middle East and its effects on prices, as well as domestic risks related to the evolution of the fiscal situation.

Recent actions by the Board of Directors of Banco de la República (JDBR) reaffirms its commitment to bringing inflation back toward the 3% target and to achieve the highest possible sustainable level of output and employment, in line with its constitutional mandate.

- Economic spending continues to exceed the productive capacity of economy, and the unemployment rate remains at historically low levels. At the same time, headline and core inflation increased, facing significant upside risks, and expectations for consumer price increases remain above the 3% target.

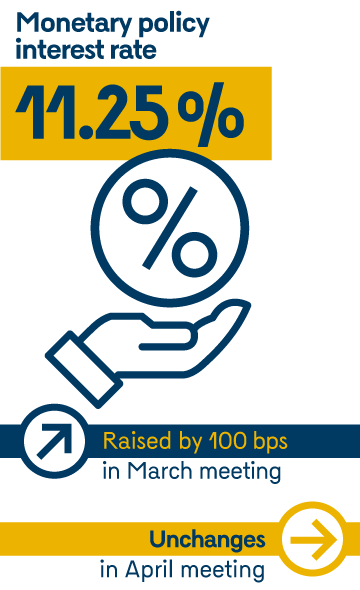

- In this context, the Board of Directors of Banco de la República raised the monetary policy interest rate by an additional 100 basis points in its March 2026 meeting, bringing it to 11.25%, and kept it unchanged at the April meeting.

- The decisions of the JDBR seek to maintain the purchasing power of the currency, particularly that of the most vulnerable population, which lacks mechanisms to protect itself against inflation.

Monetary Policy Presentation (only in Spanish)

Box Index

![]() Box 1. A 200-Basis-Point Increase in the Monetary Policy Interest Rate Between January and March 2026

Box 1. A 200-Basis-Point Increase in the Monetary Policy Interest Rate Between January and March 2026

Ospina-Tejeiro, Juan José

![]() Box 2. The New RONI: An Improved Indicator for Characterizing Climate Anomalies

Box 2. The New RONI: An Improved Indicator for Characterizing Climate Anomalies

Caicedo-García, Edgar; Vallejo-Peña, Juan Camilo

![]() Box 3. Forecast Errors and Macroeconomic Shocks in 2025

Box 3. Forecast Errors and Macroeconomic Shocks in 2025

González-Téllez, Cristian David; Pulido-Pescador, José David; Quesada-Paipa, Cristian Camilo

![]() Box 4. Estimating a Local Financial Conditions Index (FCI) for Colombia

Box 4. Estimating a Local Financial Conditions Index (FCI) for Colombia

Mora-Arbeláez, Tatiana Andrea; Herrera-Pinto, Nicolle Valentina; Moreno-Monroy, José Luis

![]() Box 5. Recent Shifts in Interest Rate Dynamics in the Colombian Economy

Box 5. Recent Shifts in Interest Rate Dynamics in the Colombian Economy

Osorio-Rodríguez, Daniel Esteban